Arlo Technologies Stock: A Hidden Gem (NYSE:ARLO) – Seeking Alpha

Michael Vi

Michael Vi

As market volatility continues, don’t miss out on the opportunity to buy small-cap stocks that have been underwater all year long. Investors have taken a risk-off attitude and leaned into defensive large-caps, but this positioning has left many smaller growth stocks (especially U.S.-focused companies that have actually seen very minimal negative impacts from the tightening macroeconomy) at very attractive valuations.

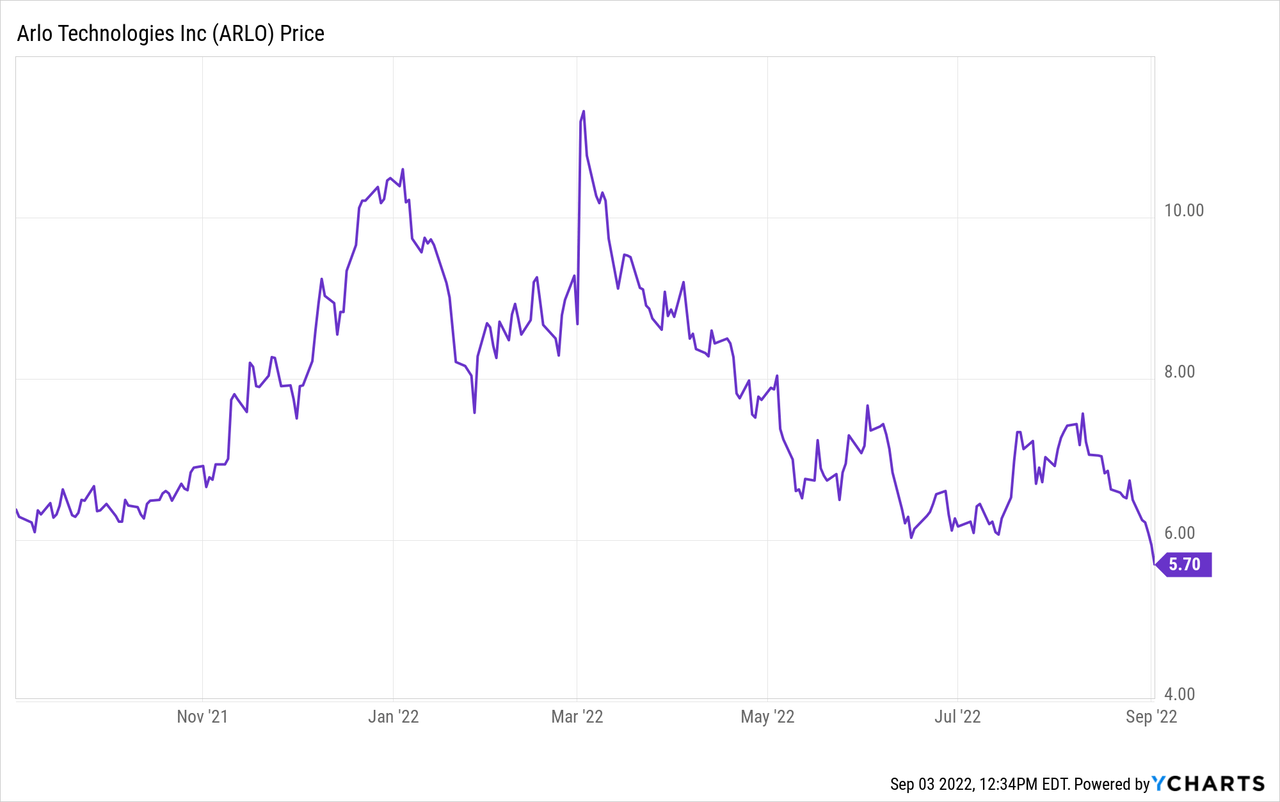

Arlo (NYSE:ARLO), the smart-camera maker that has taken on stalwarts like ADT (ADT) for home security systems, is one company worth watching. Down nearly 50% year to date, Arlo’s fundamentals have diverged entirely from its stock price, as the company has hit a streak of adding a load of new paid subscribers and posting pro forma operating profits.

A recent strong Q2 earnings print (which we’ll dive into in the next section) affirms my bullish thesis on Arlo. I continue to believe that this small-cap stock deserves a firm place in my portfolio and I’m holding on for a bigger rebound. This is especially true as the last vestiges of remote work for many companies fade, and back-to-school/back-to-office trends in September have many people reconsidering their home security plans.

Here’s a refresher of my full bull case on Arlo:

Valuation also remains extremely modest. At current share prices near $6, Arlo trades at a market cap of $500.0 million. After we net off the $135.3 million of cash on Arlo’s most recent balance sheet, the company’s resulting enterprise value is $364.7 million.

Versus Wall Street’s FY23 revenue outlook of $620.9 million (+21% y/y; data from Yahoo Finance), Arlo trades at just 0.6x EV/FY23 revenue – quite an entry-level multiple for a company that is growing gross margins and eking out profits while substantially boosting its ARR base and subscription revenue.

Stay long here and use any dips as buying opportunities.

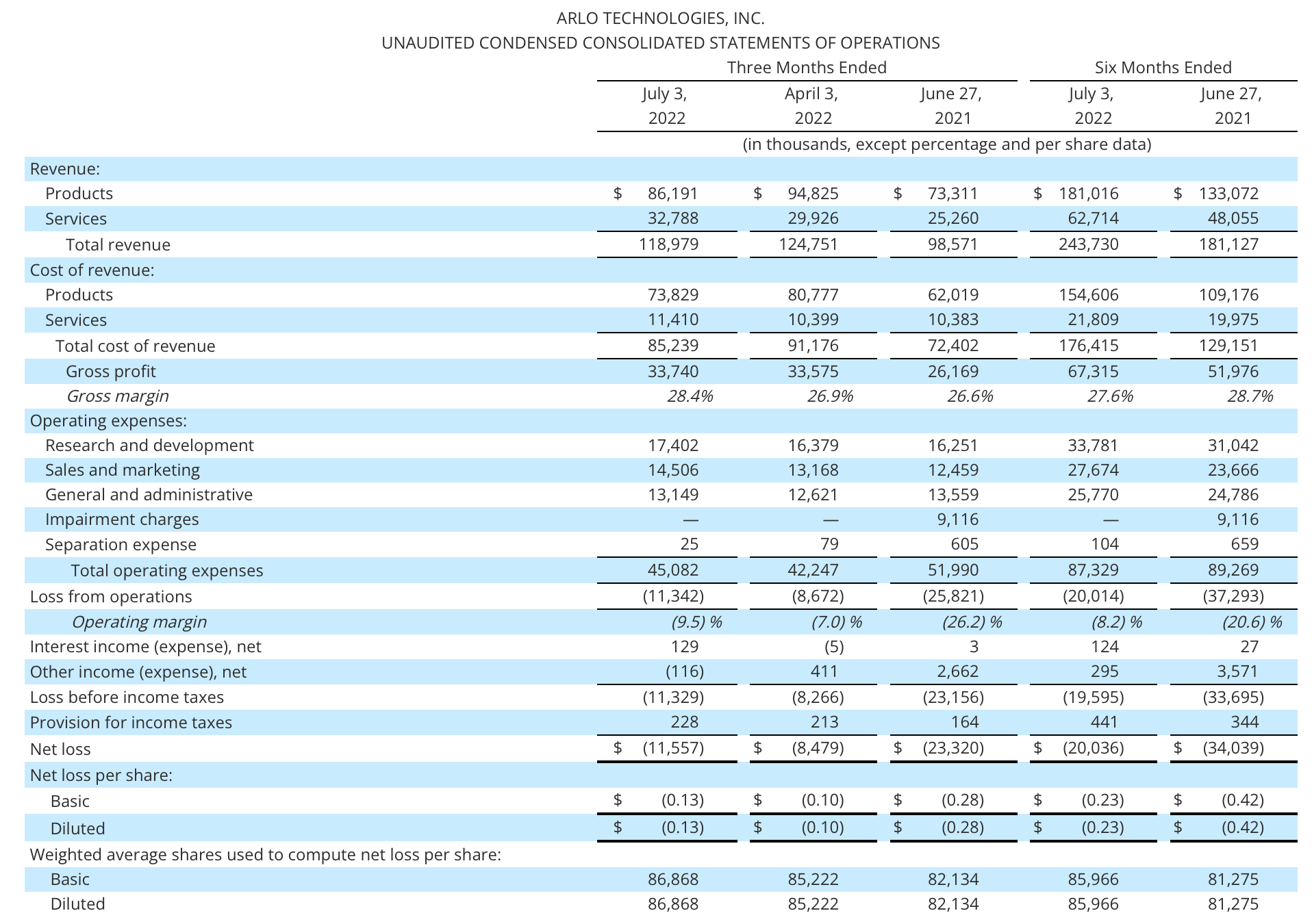

Let’s now go through Arlo’s latest Q2 results in greater detail. The Q2 earnings summary is shown below:

Arlo Q2 results (Arlo Q2 earnings deck)

Arlo Q2 results (Arlo Q2 earnings deck)

In Q2, Arlo’s revenue grew 21% y/y to $119.0 million, beating Wall Street’s expectations of $110.4 million (+12% y/y) by a huge nine-point margin. Under the hood, product (hardware) revenue grew 18% y/y while services (subscription) revenue grew 30% y/y and hit a 28% contribution to overall revenue, up from 26% in the year-ago Q2.

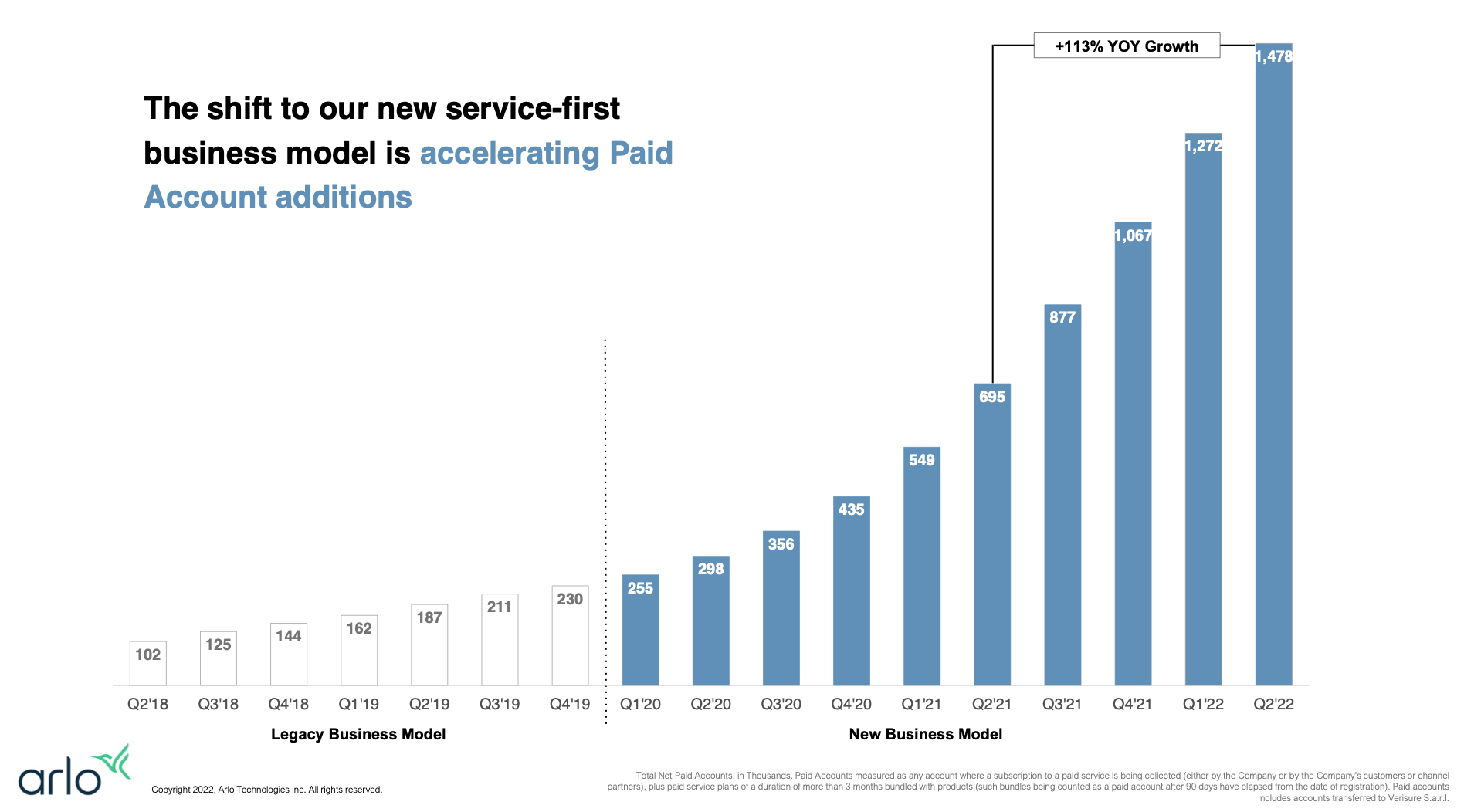

Arlo Q2 paid account growth (Arlo Q2 earnings deck)

Arlo Q2 paid account growth (Arlo Q2 earnings deck)

As shown in the chart above, the company continued to add paid accounts at a rapid clip. The company added 206k net-new accounts in the quarter, ending at 1.48 million total paid accounts, up 113% y/y. That number very slightly outpaced Q1’s 205k in net-new adds.

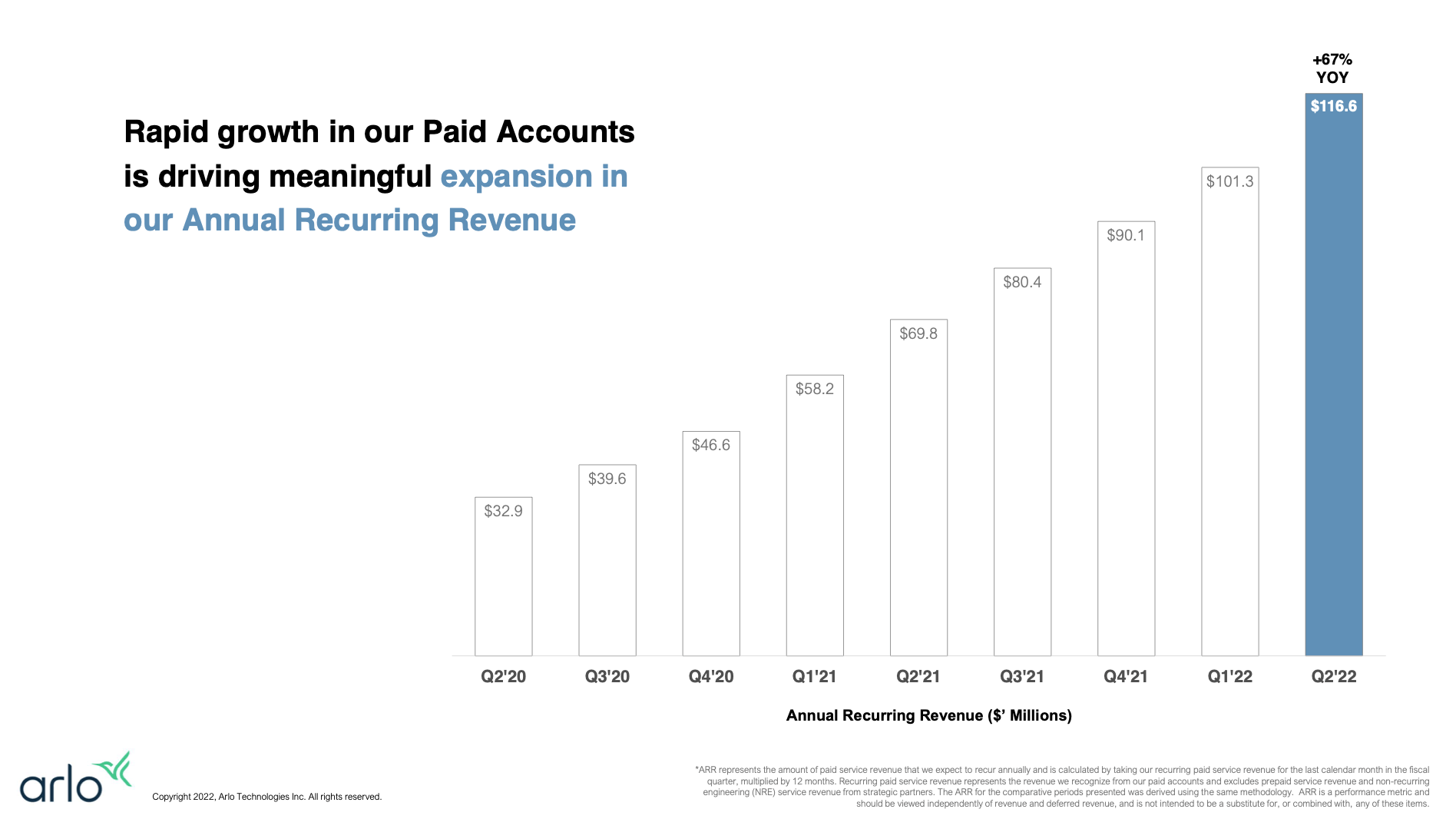

ARR, meanwhile, grew 47% y/y to $116.6 million, adding ~$15 million of net-new ARR in the quarter (versus just $11 million last quarter):

Arlo ARR deck (Arlo Q2 earnings deck)

Arlo ARR deck (Arlo Q2 earnings deck)

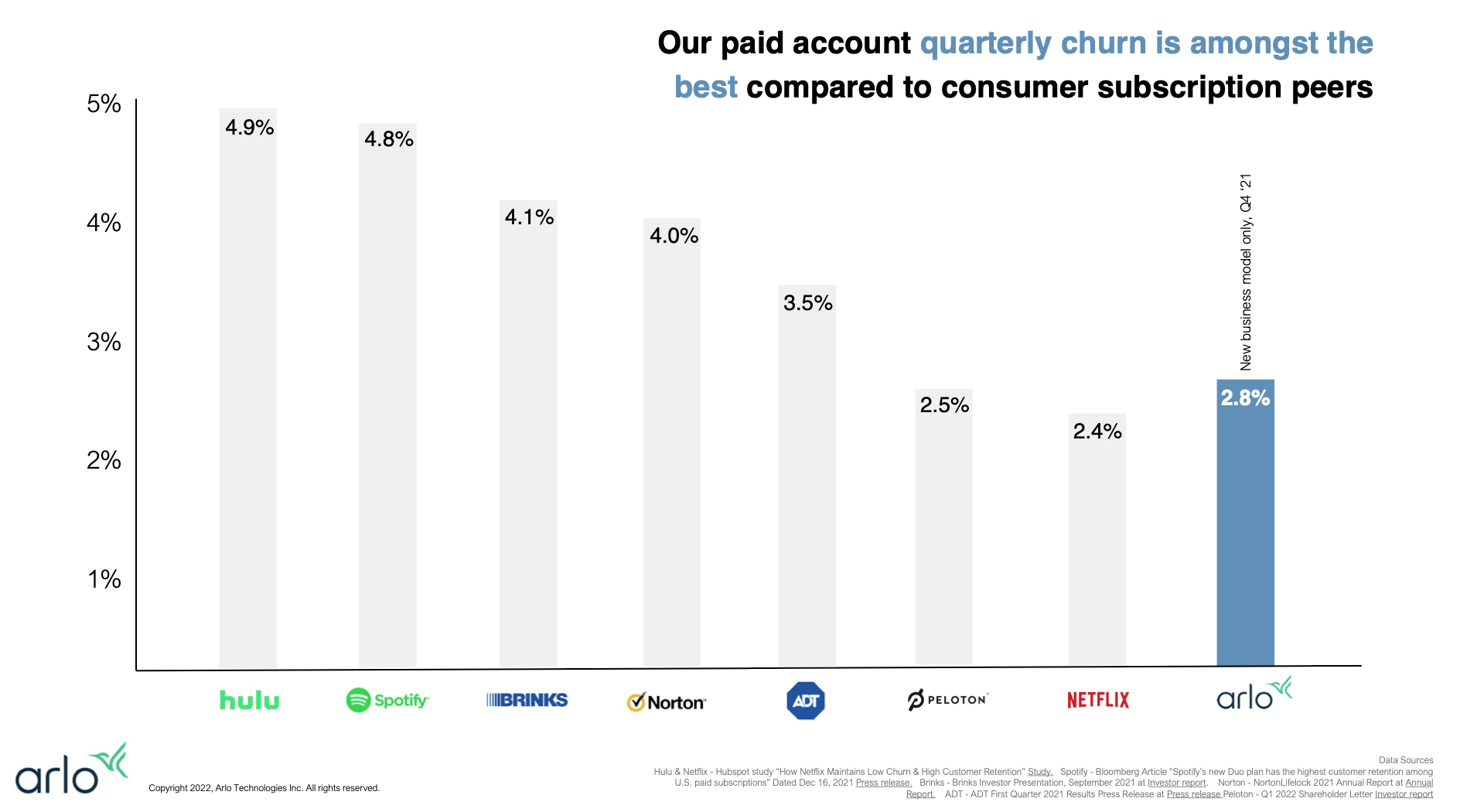

And, as shown in the chart below: Arlo also managed to hit very low churn rates for its subscription plans, with its 2.8% churn stacking much lower than many other internet services:

Arlo churn rates (Arlo Q2 earnings deck)

Arlo churn rates (Arlo Q2 earnings deck)

The company is focused aggressively on growth and brand marketing. A new campaign rolled out in Q3 is expected to deliver significant gains in sign-ups in 2023; and a new partnership in Europe is planned to deliver substantial in-region penetration. Per CEO Matthew McRae’s prepared remarks on the Q2 earnings call:

This month, we are excited to commence the rollout of our brand awareness campaign, which we will conduct in a targeted manner that focuses on new household formation to drive incremental subscription revenue. While we are kicking off the targeted marketing in Q3, we expect the bulk of the increase in POS to materialize in 2023. More information including examples of our campaign creative can be found at arlo.com/protect.

Second, we are expanding our product portfolio to address new segments and new markets. An innovative new app called Arlo Safe will provide personal protection for an individual or entire family by offering one touch emergency health, family location, and safety features, and auto crash response. And our new innovative security system will bring full sensor-based security functionality to our ecosystem of smart cameras. Both of these provide significant opportunities to drive new subscriptions, and we expect these to be available before the end of the year.

And third, Arlo will continue to broaden our routes to market. Our most prominent example of this to-date has been our Verisure relationship, which has been very successful, driving outsized growth in Europe and an impressive 46% of our Q2 revenue. We also formed a partnership with Calex last year in which Calex integrated Arlo services into their platform to broadband service providers around the country.”

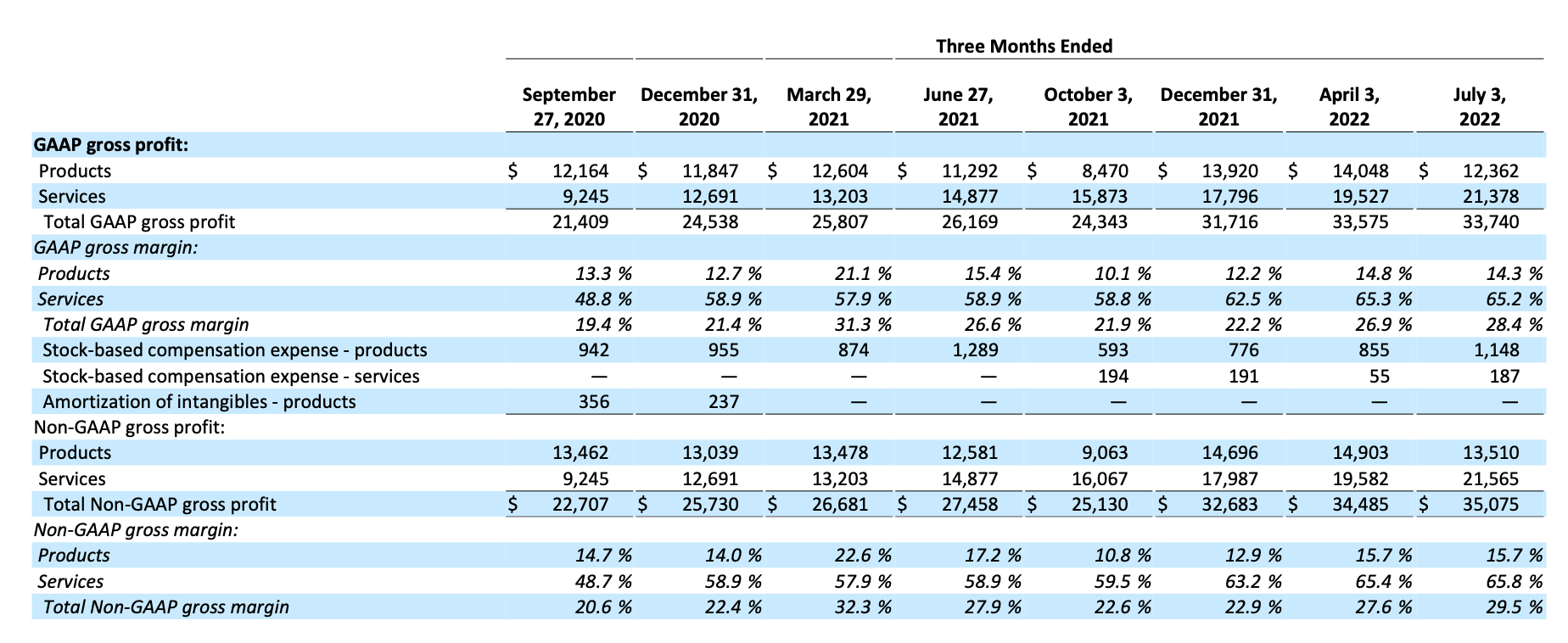

Arlo’s mix shift toward subscription services is also helping the company to consistently fit its gross margin profile. The company hit a 29.5% pro forma gross margin in the quarter, rising 190bps sequentially and 160bps y/y:

Arlo gross margins (Arlo Q2 earnings deck)

Arlo gross margins (Arlo Q2 earnings deck)

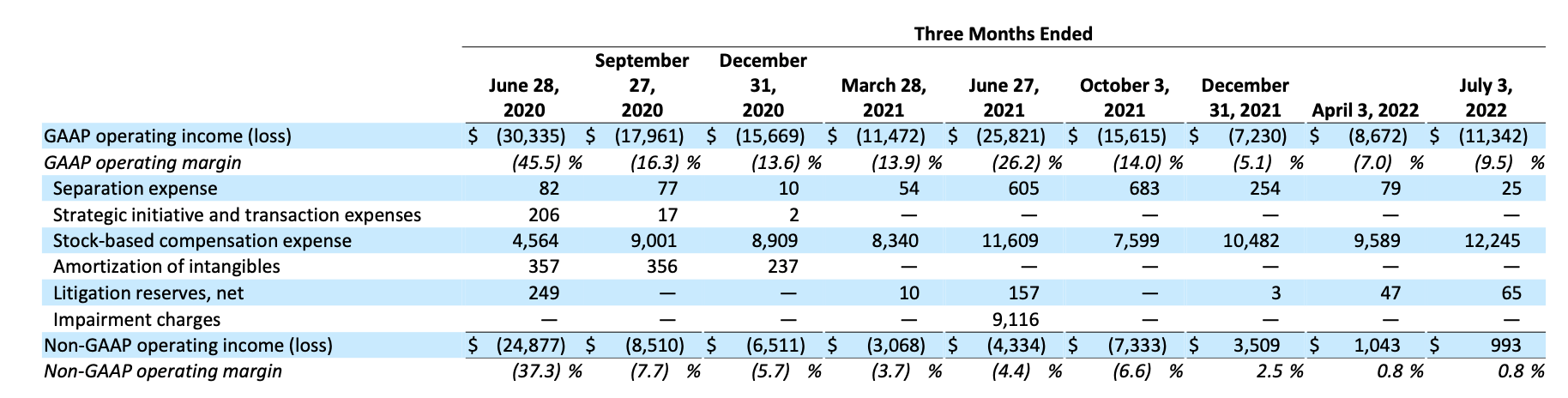

Pro forma operating margins also hit 0.8% in the quarter, up by a substantial 520bps year over year:

Arlo operating margins (Arlo Q2 earnings deck)

Arlo operating margins (Arlo Q2 earnings deck)

This improvement in profitability was driven by the richer, higher-margin revenue mix, leverage on R&D and sales costs, and the later tenure of the Verisure partnership in Europe, where the company initially paid for upfront training costs.

Investing in little-known, hard-hit small caps during market volatility is a great move for long-term oriented investors who are able to stomach short-term volatility in order to buy fantastic companies at entry-level prices. Arlo’s rebound rally will be driven by its rapidly growing subscriber base, and with plenty of initiatives in place to continue driving ARR growth, this company is hitting on all the right notes. Stay long here.

For a live pulse of how tech stock valuations are moving, as well as exclusive in-depth ideas and direct access to Gary Alexander, subscribe to the Daily Tech Download. Highly curated focus list has consistently netted winning trades of 40%+.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of ARLO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.