Array Technologies Could Be The Next Big Infrastructure Play (NASDAQ:ARRY) – Seeking Alpha

Abstract Aerial Art/DigitalVision via Getty Images

Abstract Aerial Art/DigitalVision via Getty Images

I’m not quite sure why energy production has become such a political topic, but for the purposes of this article I will be analyzing it from a strictly investing perspective. There are a wide range of views on which forms of energy the government should encourage or even whether to subsidize/penalize it at all. As investors, it behooves us to look past the “should” and instead focus on what is.

The Inflation Reduction Act (IRA) has now been put into law and it is both massive and long lasting. It fundamentally alters the profitability of energy production. Interestingly, the impacted stocks barely reacted when it got passed so I suspect some have become quite opportunistic. I set out to find the stock best positioned to benefit from the rollout.

Array Technologies (NASDAQ:ARRY), manufactures and supplies trackers for utility scale solar arrays. It is among the best positioned to benefit from the IRA.

There are a number of other solar stocks that get significant benefits from the IRA, but what sets Array apart is that it is already trading at a reasonable value at 26X next 12 month consensus earnings.

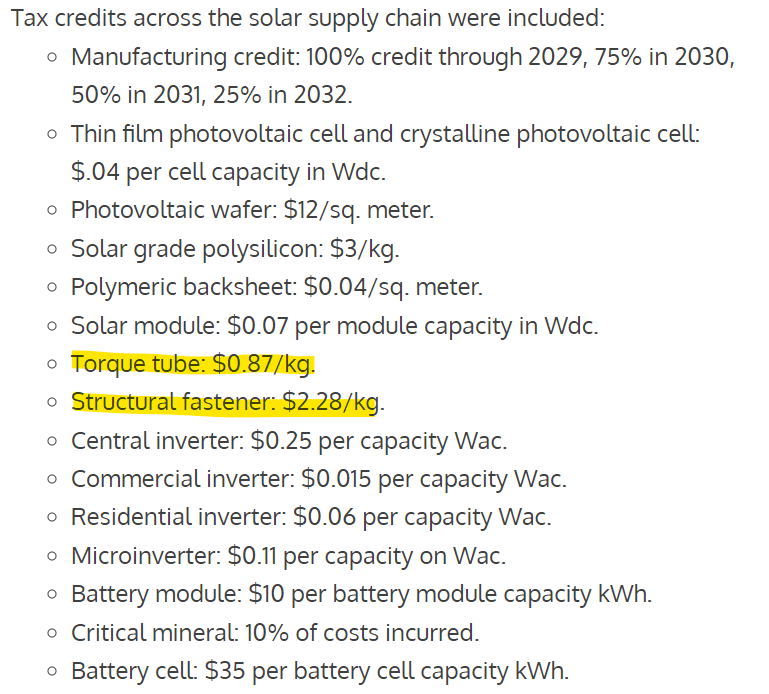

There are huge subsidies in the IRA across the entire solar supply chain. Some of the key one’s are listed below and I have highlighted the ones most relevant to ARRY.

PV Magazine

PV Magazine

Torque tubes are one of the largest revenues and expenses for Array as they make up much of the physical structure of a tracker system. Taking full note that I do not have experience procuring large steel products so I could be missing something, the subsidy appears to be nearly 100% of the cost. A quick search for tracker torque tubes shows they can be bought via Alibaba (BABA) for $630-$740 per ton.

Alibaba.com

Alibaba.com

There are 907 kilograms per ton so the IRA subsidy of $0.87 per kilogram for torque tubes gives a $789 subsidy per ton to what appears to cost $630-$740 per ton.

A couple caveats:

Steel as a commodity appears to be priced in the same ballpark at $754 U.S. dollars per ton.

Tradingeconomics

Tradingeconomics

While this subsidy level seems absurd at basically 100% of cost, it is possible the $0.87 per kilogram level was decided upon in the months when steel prices were substantially higher. During much of the negotiation of the IRA, steel prices were over $1000 per ton.

So the subsidy appears quite significant and Array can get the full amount because it does use U.S. made steel via multiple in-place supply agreements including a large recent agreement with Nucor (NUE).

In addition to torque tubes, Array makes and sells the structural fasteners that hold panels in place as they rotate to face the sun. These have a subsidy from the IRA of $2.28 per kilogram.

Finally, as an American provider of solar parts, Array contributes to a project’s eligibility for the 10% adder to income tax credits.

There are so many subsidies at so many levels of the supply chain as the building of new solar projects gets subsidized, the manufacturing of the products gets subsidized and then the actual production of the solar energy gets subsidized via the ITC and PTC (income tax credit and Production tax credit).

While each is given to a specific level of the industry vertical they will effectively be shared via pricing adjustments.

As a simple example there might be a $50 credit to one party in a transaction but the other party knows about it and wants their cut so they agree to adjust the price by $25 such that each party is functionally getting a $25 credit as compared to before the subsidy was available.

Which entity ultimately gets the lion’s share of the subsidies is the million dollar question. The company with the negotiating power due to having some sort of proprietary capability is going to be the huge winner. I don’t think I am smart enough to figure that out and hats off to those who can.

As for Array, I do think they have enough power to at least capture a significant portion of the tracker subsidies. They are among the market leaders in trackers and have significant intellectual property in both tracker designs and software. Per ARRY:

“As of December 31, 2021, the company had two U.S. trademark registrations, eleven issued U.S. patents, 152 issued non-U.S. patents, eighteen patent applications pending for examination in the United States, fourteen U.S. provisional patent applications pending, 94 patent applications pending for examination in other countries, and eight domain name registrations. Its U.S. issued patents are scheduled to expire between 2030 and 2037”

With intellectual property it is often hard to tell if there is real value there or just a slightly different design. In this case I do think ARRY has real value to its intellectual property as a competitor, Nextracker, attempted to access Array’s technology through hiring a former employee with a non-compete clause.

Array sued Nextracker and received a monetary settlement.

By having valuable IP and proving that they are willing to protect their IP in court, I think Array has what it takes to grab on to their tracker subsidies.

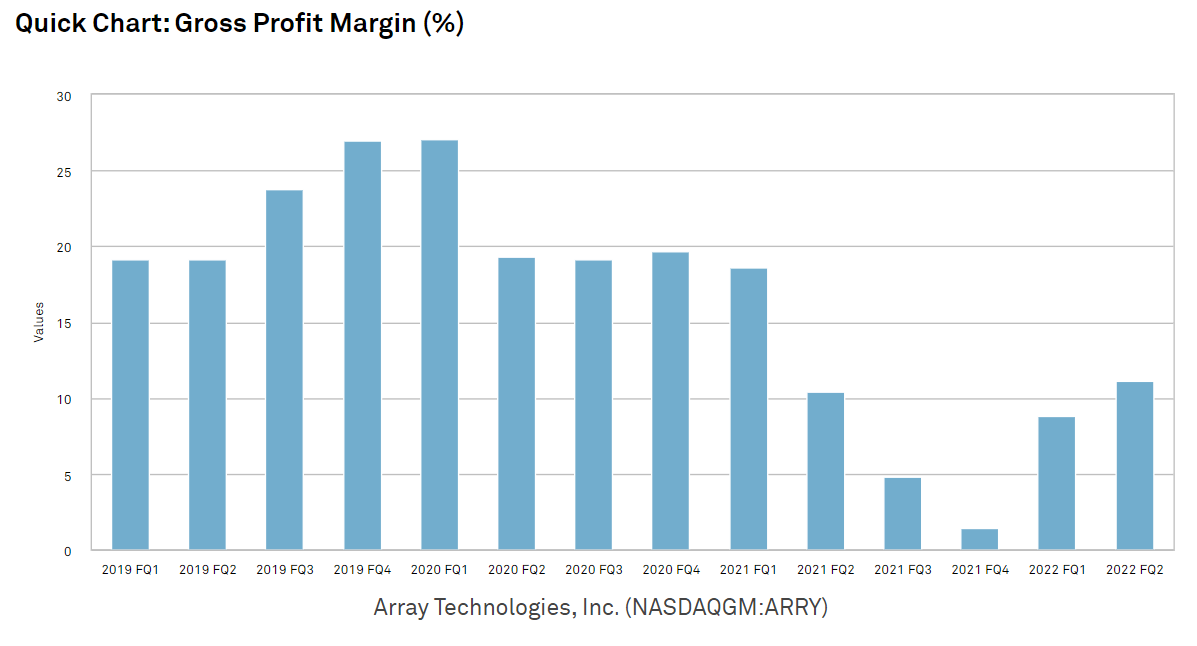

Array’s usual profit margin is around 20%. It recently fell sharply, however, as a result of the big spike in steel prices (see graph earlier in article).

S&P Global Market Intelligence

S&P Global Market Intelligence

What happened was that there was a lag time between locking in prices to Array’s customers and the actual procurement of steel. So ARRY charged their customers the appropriate price that would have been a 20% margin at the then current steel price, but then steel shot up and Array had to eat the difference.

It was a clear mistake, but Array learned and has since fixed their supply chain so as to match the pricing of their customers to the pricing at the time of procurement.

This alone is poised to return margins to their formerly higher level. On the 2Q22 earnings call CEO Kevin Hostetler said:

“we still stand by our high teens, low 20s exit rate on margins than we certainly do. We feel really good about that. We see that trajectory. I don’t think anything is changing our assumptions in that with what we see in the next 6 months or so”

At this point I think it is worth pointing out that the 2Q22 call was before the IRA was passed. Thus, the margin recovery is not coming from subsidies, but rather from the fix to their supply chain.

The aforementioned IRA subsidies have the potential to take margins much higher given their magnitude relative to the cost structure.

As of the latest quarter, ARRY had $1.9B of projects awarded or under contract:

“Total executed contracts and awarded orders at June 30, 2022 were $1.9 billion, with $1.5 billion from our Array Legacy Operations segment and $0.4 billion from STI Norland. The $1.9 billion represents an increase of 110% from June 30, 2021.”

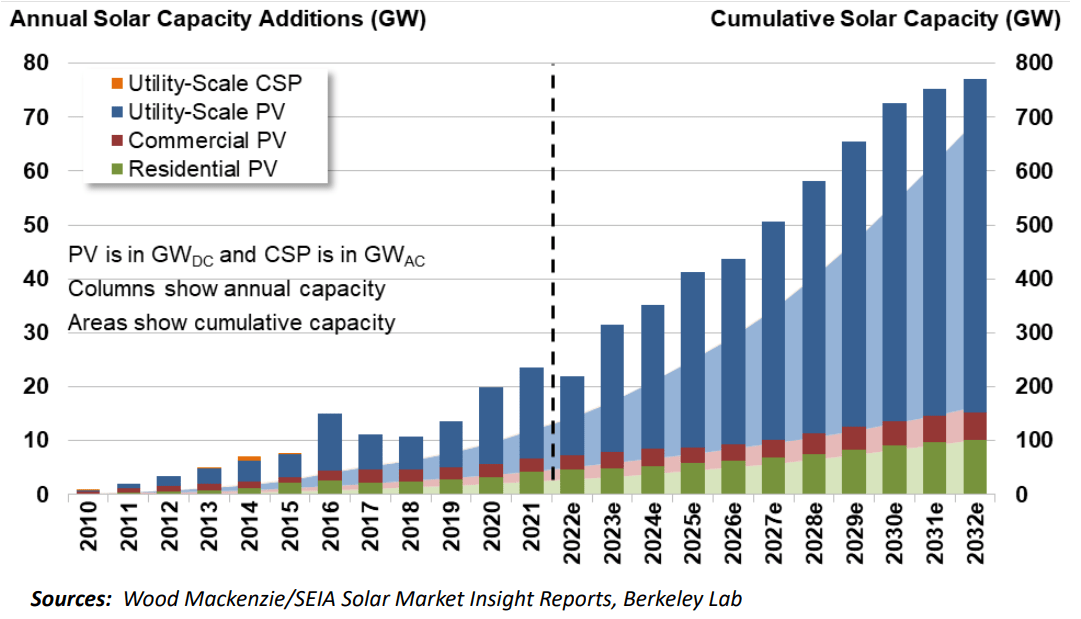

I posit that $1.9B is only the tip of the iceberg as the number of solar projects is skyrocketing. A recent study from Berkeley Labs projects ramping solar project rollout through 2032.

Berkeley Labs

Berkeley Labs

The main driver behind this is that solar is dominating energy capital spending. A certain amount needs to be spent on energy production each year to keep up with energy demand and that capital is overwhelmingly going to solar.

Berkeley Labs

Berkeley Labs

These numbers are through 2021 so they are before the stimulation of the IRA. With sizable additional subsidies that outpace the solar subsidies previously available, the forward volume of solar construction should be quite large.

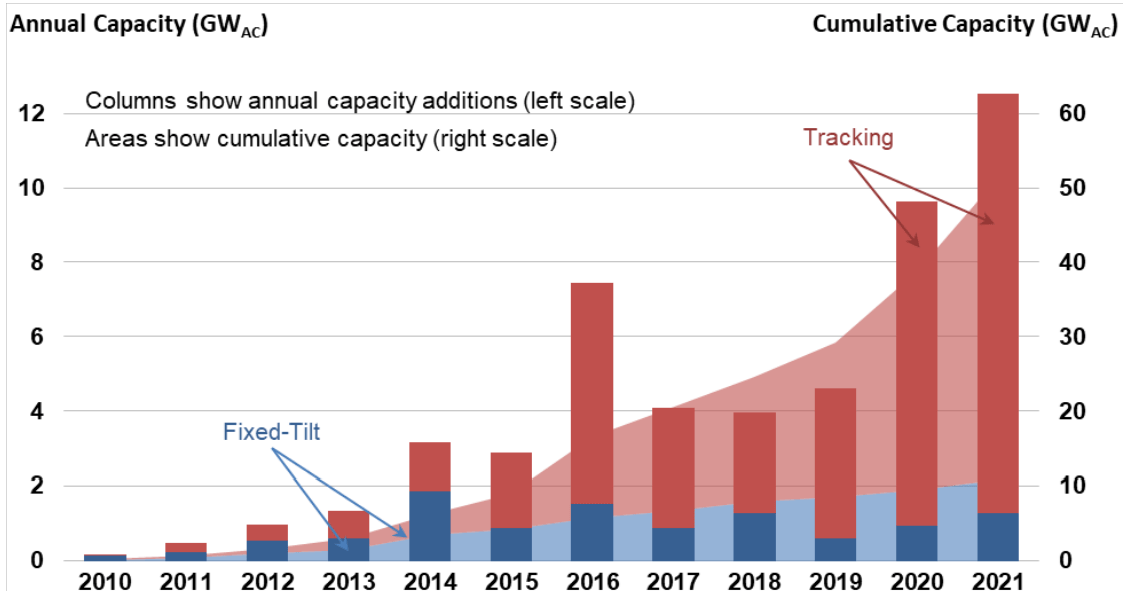

Array’s slice of this pie is the tracking systems and increasingly solar projects are being built with single axis tracking systems like the ones Array builds.

Berkeley Labs

Berkeley Labs

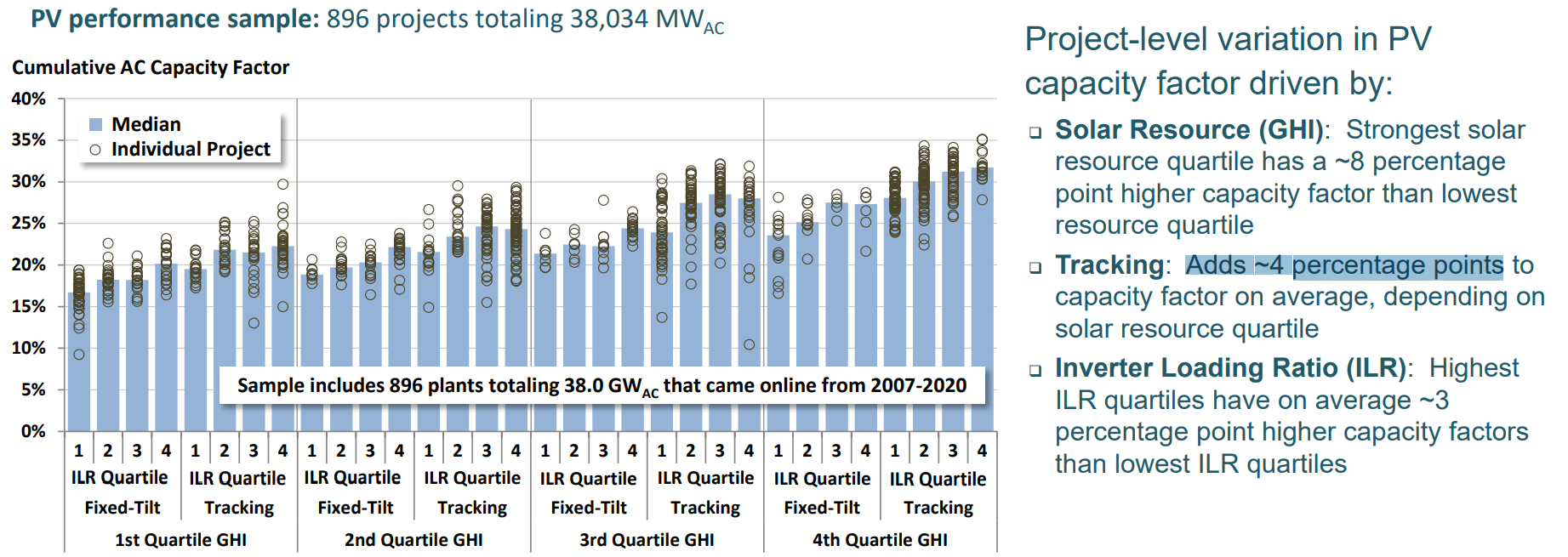

In 2021, about 90% of capacity was built with tracking and nearly all of that was single axis.

Trackers are quite cost effective since they are not terribly expensive but substantially increase the efficiency of the panels. On average, trackers add 4 percentage points to capacity factor.

Berkeley Labs

Berkeley Labs

That may not sound like much, but 4 percentage points when capacity factor is otherwise around 20% is a roughly 20% increase in output of the panels.

So going forward, here is how I see demand.

Solar projects were plentiful in 2021 and were expected to ramp up due to demand. The tax incentives provided in the IRA make solar projects more profitable for the entire supply chain. That represents a positive shift in the supply curve. Basic economics teaches us that a positive shift in the supply curve increases the overall quantity of units produced.

Additionally, an increasing percentage of solar arrays are being built with trackers. Thus, Array Technologies is getting a slightly bigger percentage of a much bigger pie.

This increased volume should have amplified impacts on bottom line earnings because Array is on the cusp of 2 sources of margin increase.

Higher revenues at higher margins means much higher earnings.

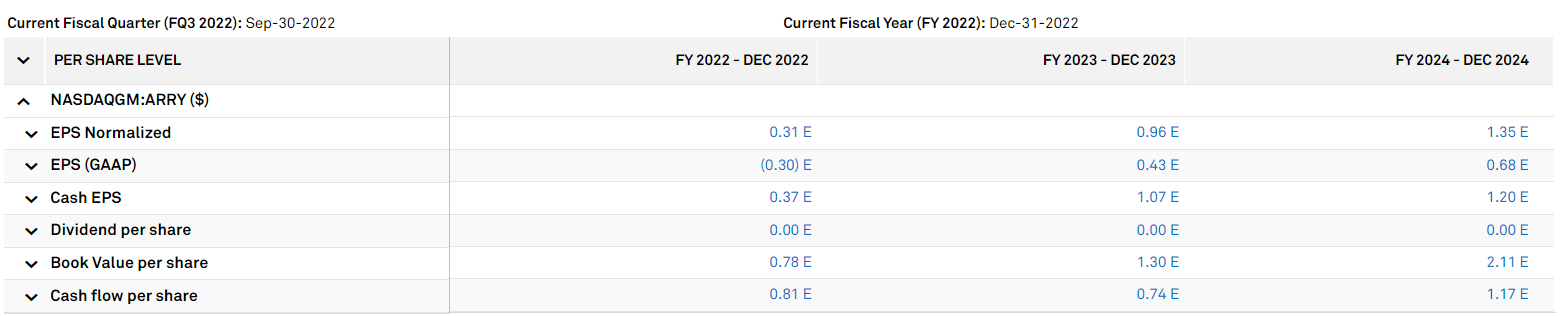

Indeed, consensus estimates reflect this with normalized, GAAP, and Cash earnings expected to climb to $1.35, $0.68, and $1.20 by 2024, respectively.

S&P Global Market Intelligence

S&P Global Market Intelligence

That level of growth makes Array undervalued at $17.53. Current multiples are quite low relative to other companies with that pace of growth.

I think there is potential for ARRY to beat consensus estimates as most of the estimates came out before the IRA was passed.

Various parts of the solar development process require skilled labor which is in short supply. This may slow the development pipeline.

At this point it is highly unclear who will capture the value provided by the subsidies. Default assumption is that it will be shared among industry participants as well as the end user, but that could change as bottlenecks emerge.

Make your money work for you

At Portfolio Income Solutions we do the rigorous analysis to determine which stocks will work and which won’t. We then curate a portfolio of the most opportunistic individual stocks and provide members with continuous analysis to help keep their investments in shape. We constantly watch the market in order to buy and sell the right stocks at the right times.

Start investing with the aid of dedicated research by joining Portfolio Income Solutions.

Not sure yet? Grab a free trial. Canceling is easy and there are no obligations.

This article was written by

2nd Market Capital Advisory specializes in the analysis and trading of real estate securities. Through a selective process and consideration of market dynamics, we aim to construct portfolios for rising streams of dividend income and capital appreciation.

Our Portfolio Income Solutions Marketplace service provides stock picks, extensive analysis and data sheets to help enhance the returns of do-it-yourself investors.

Investment Advisory Services

We now offer a way to directly invest in our Proprietary Investment Portfolio Strategy via REIT Total Return, which replicates our activity in client accounts. Total Return client’s brokerage accounts are automatically invested simultaneously and at the same price when we make a trade in the REIT Total Return Portfolio (also known as 2CHYP).

Learn more about our REIT Total Return Portfolio.

Dane Bowler, along with fellow SA contributors Simon Bowler and Ross Bowler, is an investment advisory representative of 2nd Market Capital Advisory Corporation (2MCAC). As a state registered investment advisor, 2MCAC is a fiduciary to our advisory clients.

Full Disclosure. All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of the specific person. Please see our SA Disclosure Statement for our Full Disclaimer.

Disclosure: I/we have a beneficial long position in the shares of ARRY either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Important Notes and Disclosure:

All articles are published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.

The information offered is impersonal and not tailored to the investment needs of any specific person. Readers should verify all claims and do their own due diligence before investing in any securities, including those mentioned in the article. NEVER make an investment decision based solely on the information provided in our articles.

It should not be assumed that any of the securities transactions or holdings discussed were profitable or will prove to be profitable. Past Performance does not guarantee future results. Investing in publicly held securities is speculative and involves risk, including the possible loss of principal. Historical returns should not be used as the primary basis for investment decisions.

Commentary may contain forward looking statements which are by definition uncertain. Actual results may differ materially from our forecasts or estimations, and 2MC and its affiliates cannot be held liable for the use of and reliance upon the opinions, estimates, forecasts, and findings in this article.

S&P Global Market Intelligence LLC. Contains copyrighted material distributed under license from S&P

2nd Market Capital Advisory Corporation (2MCAC) is a Wisconsin registered investment advisor. Dane Bowler is an investment advisor representative of 2nd Market Capital Advisory Corporation.