Byrna Technologies: Growth Is Fading, Profitability Out Of Reach – Seeking Alpha

KanawatTH

KanawatTH

In April 2021, I wrote a bullish article on SA about non-lethal weapon maker Byrna Technologies (NASDAQ:BYRN) in which I said that it had an interesting product as well as rapidly growing sales.

The company’s share price soared by about 50% over the next few months but has been falling ever since and Byrna is valued at $182.3 million as of the time of writing. The company’s growth has declined significantly despite much higher marketing spending, and inventories are at concerning levels. In addition, there don’t seem to be further economies of scale and net cash used in operating activities came in at $12.8 million for the first nine months of 2022.

Overall, I’m bearish on Byrna and I think that the significant increase in the market valuation since September provides a good exit point for investors. Let’s review.

In case you haven’t read my previous article about Byrna, here’s a short description of the business. The company specializes in the manufacturing and sale of non-lethal self-defense devices and its main product is Byrna SD – a CO2 gun that can fire pepper-filled rounds at up to 60 feet.

Byrna

Byrna

One of these paper kits costs $400, compared to $359 when I first covered Byrna. The company also sells body armor, personal safety alarms, and apparel products. The projectiles that are currently available for Byrna SD consist of natural pepper, pepper and tear gas, and plastic. In addition, the company offers training and recreational projectiles that are water-soluble. In May 2022, Byrna expanded its product offering into defensive pepper sprays through the acquisition of Fox Labs International for $2.2 million.

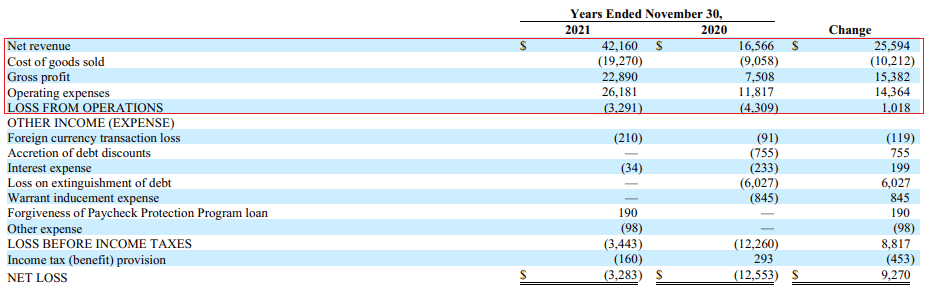

Turning our attention to the financial performance of the business, among the key factors I liked Byrna in 2021 was its high sales growth rate. As I mentioned in my previous article, the company expected to book revenues of $33-$38 million in FY21, which was double the level from the previous year. Well, Byrna finished FY21 with revenues of $42.2 million as it shipped over 88,000 orders and daily web sessions at Byrna.com topped 20,000. In addition, the gross profit margin grew from 45.3% to 54.3% and the loss from operations shrank to $3.3 million from $4.3 million.

Byrna

Byrna

In my view, marketing played a key part in the expansion of the business as marketing and advertising related costs soared to $2.7 million from $1 million.

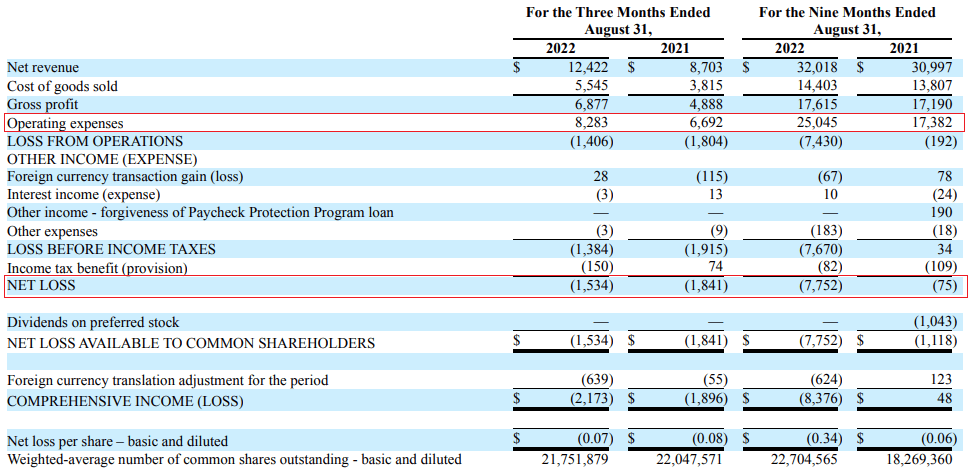

Unfortunately for investors, it appears that this was as good as it gets. With high inflation rates in the US hitting demand for discretionary goods, Byrna’s revenues barely grew during the first nine months of FY22 despite an increase in marketing expenses from $1.3 million to $3.9 million. The situation looks even worse when you take into account that Fox Labs accounted for $0.41 million of the revenues for the nine months ended August 31, 2022. In addition, the gross profit margin inched down to 55% from 55.5% and the net loss soared to $7.75 million as payroll related costs rose by $3 million to $12.6 million. Adjusted EBITDA thus swung from $2.78 million to negative $2.4 million.

Byrna

Byrna

With inflation rates remaining stubbornly high, Byrna’s forecasts for its growth are also softening. In October, the company said that it expects revenues of $16 million to $18 million for Q4 FY22 and that growth in FY23 would be 10% – 30%. In my view, even these figures could be too optimistic, but the more pressing issue is that increased spending on marketing seems to have an inconsequential effect and there is no clear path forward to reaching profitability. In light of the current macroeconomic environment, I’m bearish on Byrna in the short term.

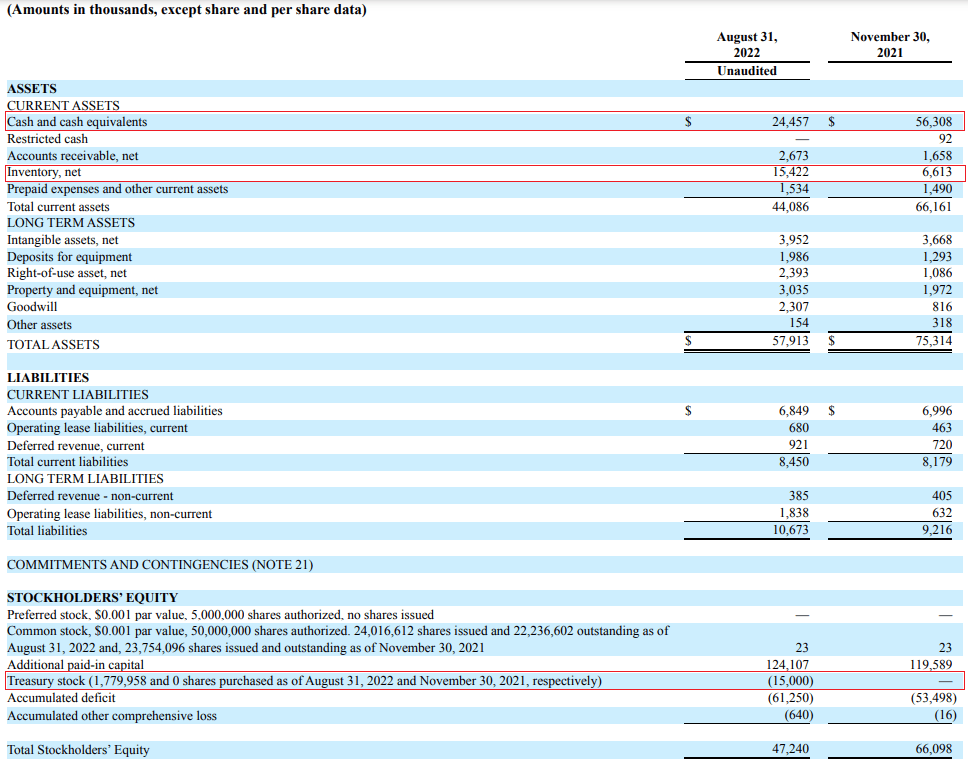

Turning our attention to the balance sheet, I think the situation is starting to look concerning as cash and cash equivalents were down to $24.5 million as of August and net cash used in operating activities in the nine months ended August was $12.8 million. During the period, Byrna spent $15 million on share buybacks and inventory soared to $15.4 million despite a backlog of unshipped orders at the end of the quarter of just $1.65 million.

Byrna

Byrna

Overall, I think that it’s highly likely that we are in the early innings of a global recession and companies selling discretionary goods such as Byrna will have a tough time. Considering the market valuation of the company has almost doubled since the end of September, this could be a good time for investors to trim or close their positions. According to data from Fintel, the short borrow fee rate is just 0.98% as of the time of writing. However, call options look somewhat expensive and I think short selling could be dangerous. It could be best for risk-averse investors to avoid Byrna.

Seeking Alpha

Seeking Alpha

Looking at the risks for the bear case, I think that there are two major ones. First, I could be overestimating the effect of high inflation on Byrna’s sales and revenue growth rates pick up over the coming months. Second, the share prices of microcap companies can increase for spurious and unknown reasons.

This is a challenging year for Byrna as revenue growth is much lower despite a significant increase in marketing spending. In addition, the gross margin has stopped growing and profitability seems to be out of reach as payroll expenses are also rising rapidly.

Byrna has spent $15 million on share buybacks but I’m concerned this could’ve been a bad move considering cash was down to $24.5 million as of August and net cash used in operating activities in the nine months ended August was $12.8 million.

In my view, risk-averse investors should avoid this stock.

If you like this article, consider joining Bears and Resources. I post my portfolio and shortlist there and you can also find exclusive ideas from our community of investors. I like to focus on undervalued companies that the market is ignoring, like an island of misfit toys. Both long and short ideas.

So, what can you expect to get from this service?

This article was written by

I have been investing in stocks for 13 years now, most of the time in my native Bulgaria. I have a bachelor’s degree in Finance and a Master’s degree in International Business and I like reading Pratchett and Michael Lewis. Regarding the opportunities that I cover, please take into account that I’m an admirer of legendary fund manager Peter Lynch so I tend to follow a lot of his investment philosophy.

– Disclosure: I am not a financial adviser. All articles are my opinion – they are not suggestions to buy or sell any securities. Perform your own due diligence and consult a financial professional before trading.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I am not a financial adviser. All articles are my opinion – they are not suggestions to buy or sell any securities. Perform your own due diligence and consult a financial professional before trading.