HP Inc. Stock: Warren Buffett Bought A Computer Stock! (NYSE:HPQ) – Seeking Alpha

Justin Sullivan/Getty Images News

Justin Sullivan/Getty Images News

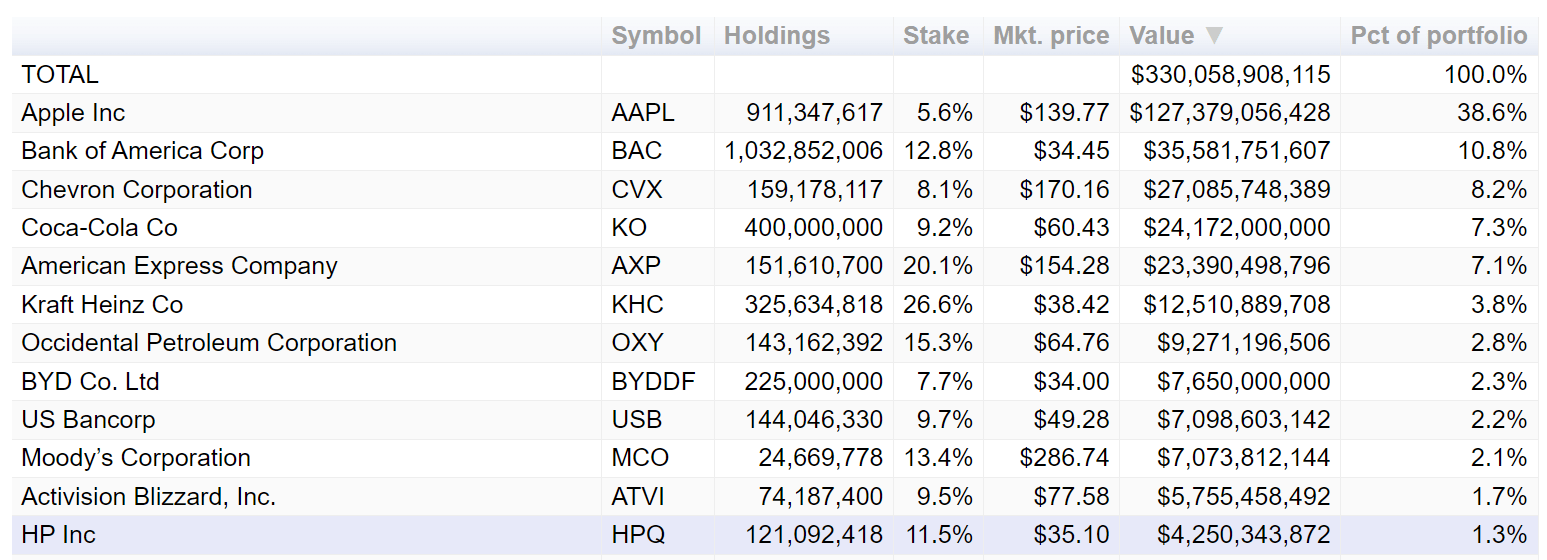

Berkshire Hathaway’s recent 13F disclosure shows that Warren Buffett created a sizable position in HP Inc. (NYSE:HPQ). The position is worth about $4.3B as of this writing and is the 12th largest position in BRK’s enormous equity portfolio. You might be wondering why Buffett, who repeatedly said he won’t invest in tech stocks because he does not understand tech stock, suddenly created a large position in a computer company now.

This article will show that under its technology surface, HPQ is actually an exemplary Buffett-type business. It demonstrates all the traits of a perpetual compounder that Buffett seeks: superb profitability and return on capital, financial flexibility, strong cash flow but low maintenance CAPEX requirements, generous shareholder returns, et al. Finally, its current valuation also fits what I call Buffett’s 10x pretax rule, as shown immediately next.

Source: cnbc.com/berkshire-hathaway-portfolio/

Source: cnbc.com/berkshire-hathaway-portfolio/

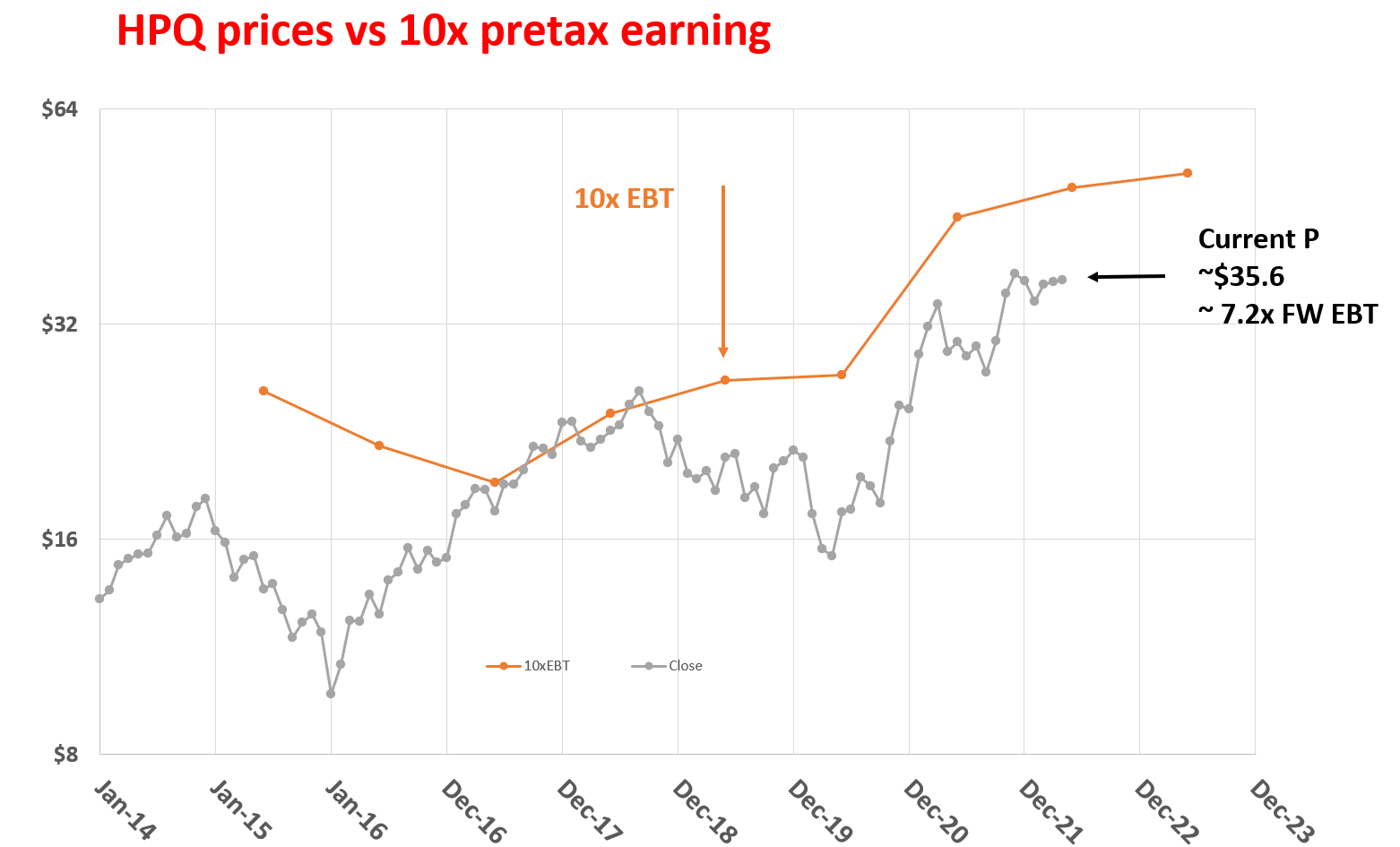

According to Buffett’s 10x pretax rule, HPQ is now a wonderful firm for sale at a wonderful price, as shown in the chart below. The figure compares HPQ’s historical price and its 10x pretax earnings (also referred to as EBT, Earnings Before Taxes). As seen, if the price has risen near or above 10x EBT, it has been a good time to sell like in 2016 and 2017. And vice versa, when the price fell below 10x EBT, it has been a favorable time to buy. And now, with a valuation of 7.2x FW EBT, is such a favorable time to buy. As to be detailed next, at 7.2x EBT, even if HPQ’s profits remain stagnated indefinitely, the investment would already produce an almost 14% pretax yield, comparable to a 14% equity bond.

Source: author based on Seeking Alpha data

Source: author based on Seeking Alpha data

In case you are new to Buffett’s 10xEBT rule, I have a free blog article to provide all the details plus all the Q&A I’ve received. A quick summary to facilitate the ease of reference:

So with this framework, let’s examine HPQ more closely.

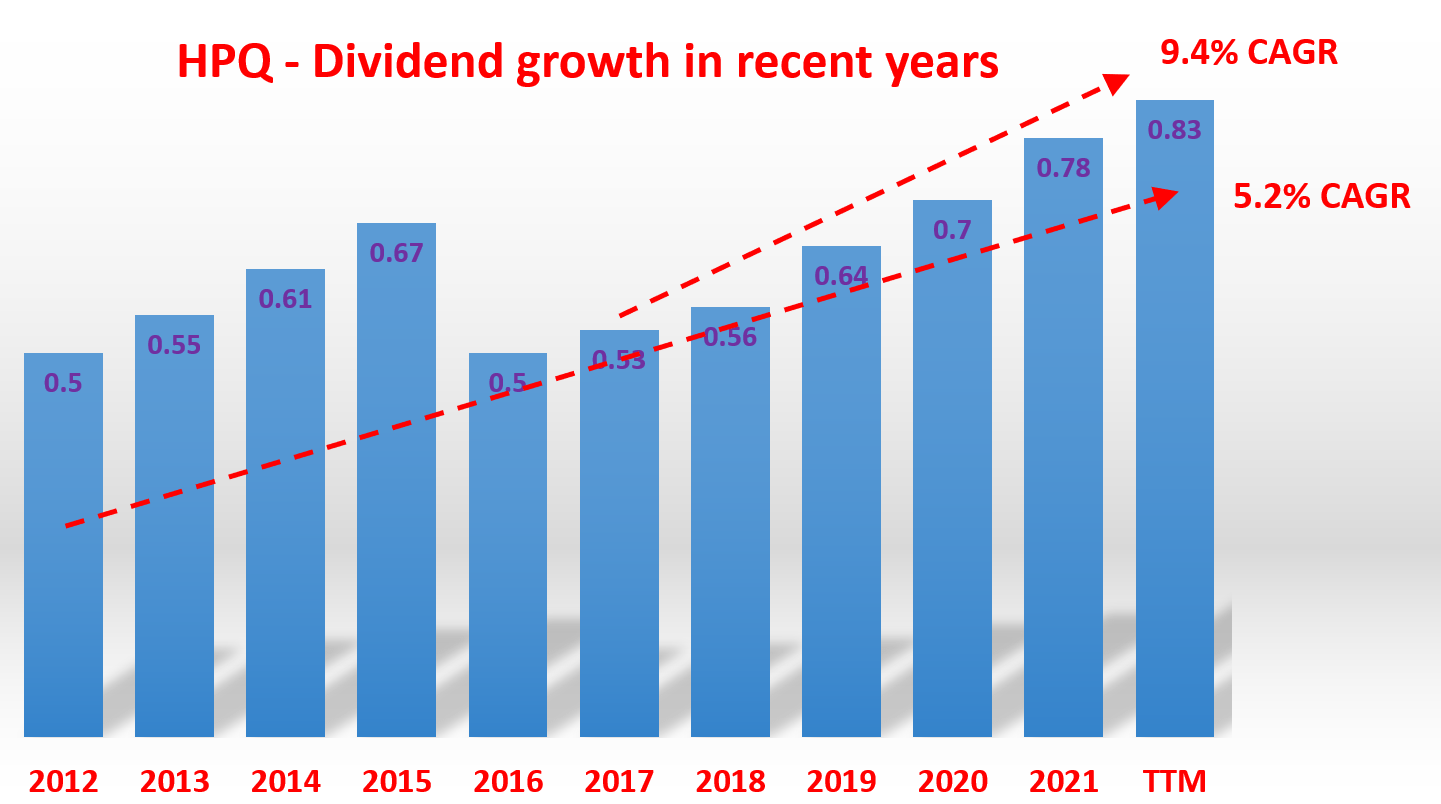

As detailed in our blog article, a shortcut to looking into the short-term existential issue is the dividend, the most reliable indicator of a business’s profit.

As shown below, HPQ has been paying dividends for years. Despite the hiccups between 2015 and 2016, the dividends have shown a general growing trend. The growth rate during the past decade has been a healthy 5.2% CAGR, and in the past 5 years have been almost 10%.

Another reliable metric is interest coverage and financial strength. The business currently carries long-term debt of about $6.4B. Its total interest expenses are about $252M and its effective tax rate is about 13.5%. As such, the business’s debt coverage (defined as EBIT divided by interest expenses) is about 17x, essentially debt-free.

Source: author based on Seeking Alpha data

Source: author based on Seeking Alpha data

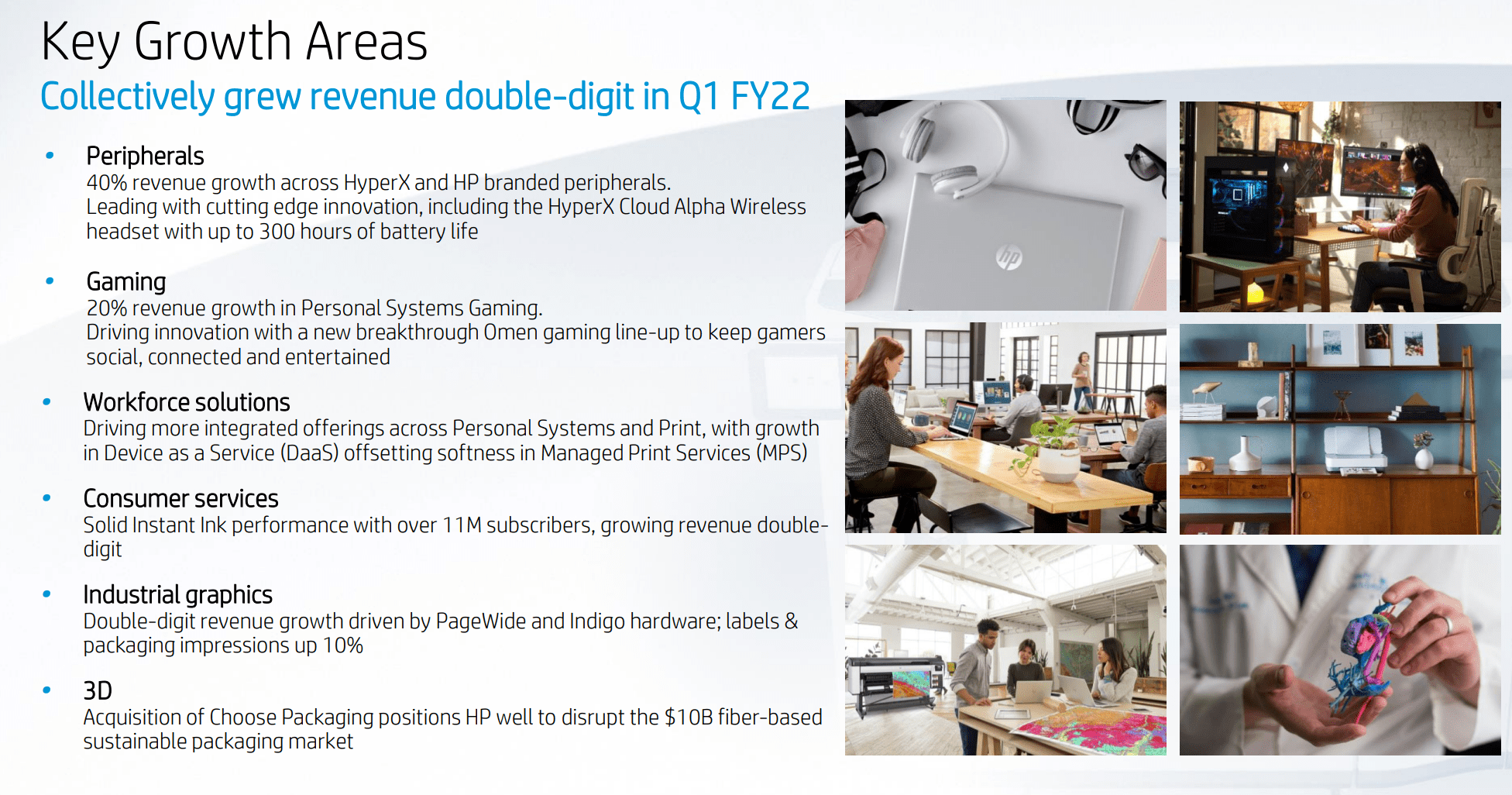

In the long term, existential issue ultimately is a largely subjective judgment. To me, HPQ’s core business caters to a society’s need that extends indefinitely into the future: our basic computing, working, and gaming needs. Even within its mature businesses, there are some prospects for the top line albeit slowly. But again, at its current valuation of 7.2x EBT, the return on investment would already be double-digit if there is no growth. Product cycles for PCs and printers aren’t as important as they previously were, but a slow secular growth can still be expected in the low-single-digit range in the long term.

At the same time, there are signs of higher-growth and higher-margin areas. Notably, it just posted 20% revenue growth in Personal Systems Gaming. Gamers spend generously and sometimes even uncontrollably on their gears – and I, unfortunately, have to experience this firsthand as the parent of a teenage kid – such as cameras, speakers, and headsets. Its new breakthrough such as Omen can fuel further growth as it integrates the social network aspects and keeps gamers connected.

HPQ earnings report

HPQ earnings report

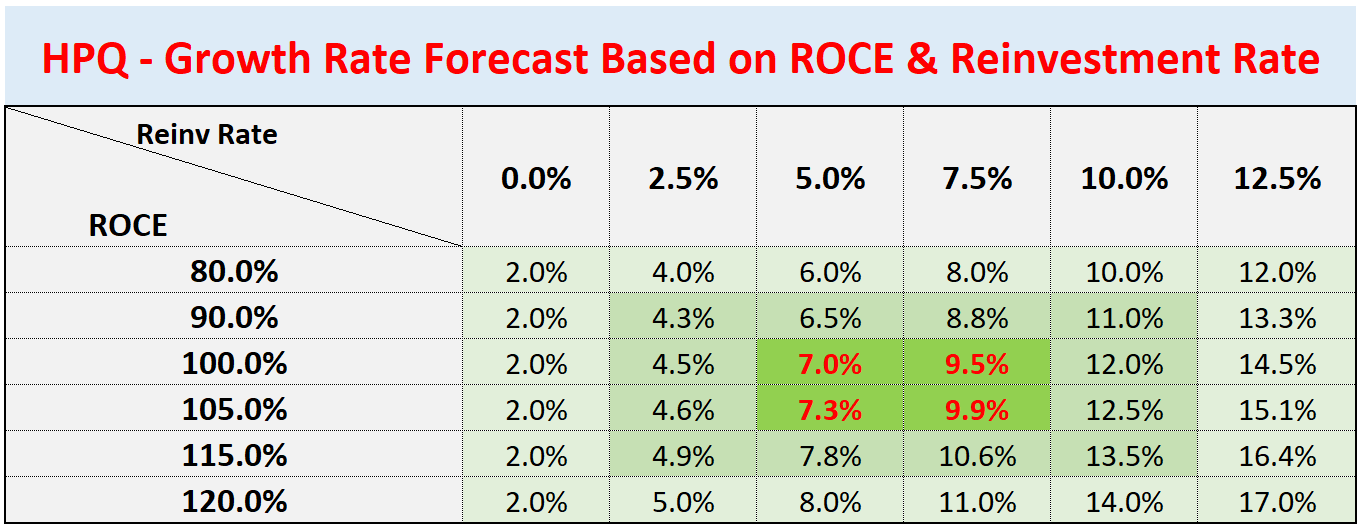

As detailed in my free blog article, in the long term, the growth rate is simply given by the product or ROCE (return on capital employed) and reinvestment rate.

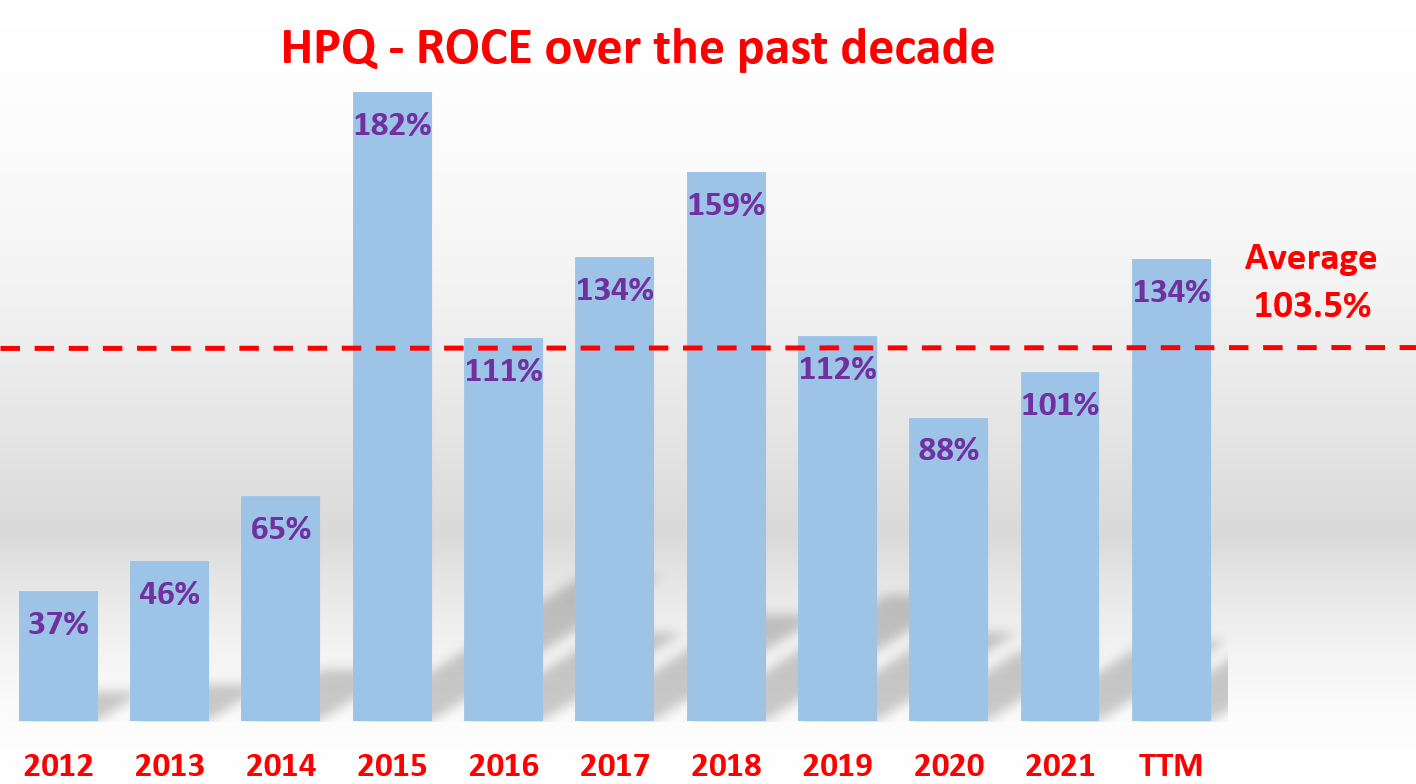

HPQ was able to maintain superbly high ROCE over the past decade as you can see from the following chart. It has been on average 103.5% for the past decade. And note that this average has already been biased by the lower profitability it experienced between 2012 to 2014, when the ROCE hovered between 37% to 65%. Since 2015, its ROCE has been consistently and substantially above 100% with the exception of 2020 when it dipped slightly to 88%.

Source: author and Seeking Alpha.

Source: author and Seeking Alpha.

For reinvestment rate, HPQ enjoys strong cash generation and capital allocation flexibility as you can see from the following highlights taken from its most recent earnings report:

All told, HPQ on average spent only about 13% of operating cash flow on maintenance CAPEX in recent years, about 20% on dividends, and has been maintaining a reinvestment rate between 5% to 7.5% in recent years.

We can now estimate the long-term growth rate using both the ROCE and the reinvestment rate obtained above, as illustrated in the next table. Note that I adjusted the growth rate by 2.5 percent for inflation. As seen, to me, the most likely growth scenario in the long-term would an annual growth rate in the upper-single digit, between 7.0% to 9.5%.

Now to put the pieces together and conclude:

Source: author.

Source: author.

This article analyzes HPQ, the newest large addition into BRK’s equity portfolio. Beneath its technology surface, it is a textbook Buffett investment featuring a high return on capital (over 100% on average in recent years), strong cash generation yet low cash requirement (on average only needs 13% of operating cash flow as maintenance CAPEX), and generous shareholder returns ($1.5B repurchases during the past quarter plus $0.3B of dividends). And this industry leader in the personal computing space is now for sale at only 7.2x EBT.

Finally, risks. HPQ faces both macroscopic risks and also risks unique to itself. The effects of the COVID-19 pandemic represent a major risk. The actions taken by governments, businesses, and individuals in response to the situation are completely unpredictable. For HPQ itself, it relies on third-party suppliers and a global distribution network. Such reliance creates risks including component shortages and supply chain. The Ukraine-Russia war and pandemic can create further complications.

Thx for reading! Look forward to your comments and thoughts!

Check out our marketplace service

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 2x in-depth articles per week on such ideas.

We have proven and perfected our methods with our own money and efforts for the past 15 years. For example, our aggressive growth portfolio has helped ourselves and many around us to maximize return with minimal drawdowns.

Lastly, do not hesitate to take advantage of the free-trials – they are absolutely 100% Risk-Free.

This article was written by

** Disclosure** I am associated with Envision Research

I am an economist by training, with a focus on financial economics. After I completed my PhD, I have been professionally working as a quantitative modeler, with a focus on the mortgage market, commercial market, and the banking industry for more than a decade. And at the same time, I have been managing several investment accounts for my family for the past 15 years, going through two market crashes and an incredible long bull market in between.

My writing interests are mostly asset allocation and ETFs, particularly those related to the overall market, bonds, banking and financial sectors, and housing markets. I have been a long time SA reader, and am excited to become a more active participator in this wonderful community!

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.