SoFi: Irrational Hit (NASDAQ:SOFI) – Seeking Alpha

Justin Sullivan

Justin Sullivan

After an odd selloff following strong Q3’22 earnings, SoFi Technologies (NASDAQ:SOFI) is poised to finish the rally the stock started. The fintech has been maligned for not taking charges on loans held on the balance sheet, but the company is poised to benefit whether holding or ultimately selling the personal loans. My investment thesis remains ultra bullish on the growth story for SoFi.

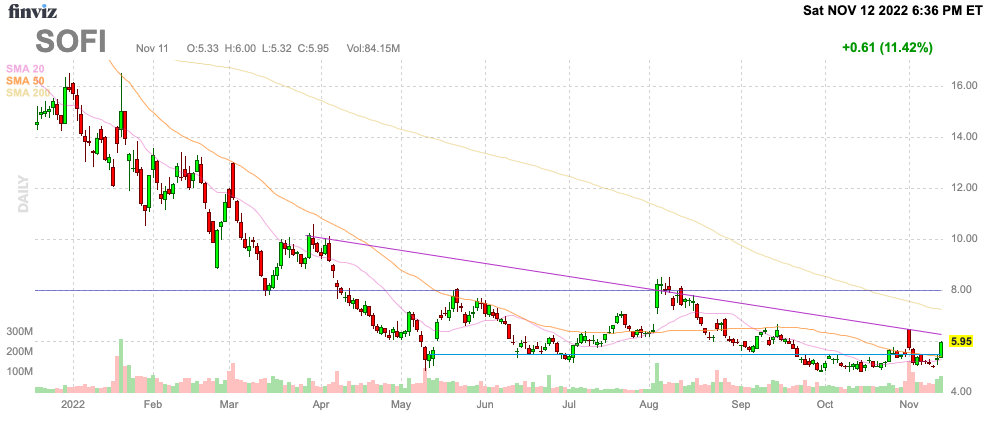

Following Q3’22 earnings pre-market on November 1, SoFi initially rallied to over $1 to a high of $6.47. The stock was up 19% on the day at the peak and barely ended up positive for the day. In days, SoFi was trading below the pre-earnings price and dipped below $5 despite the fintech guiding up expectations for the year.

Source: FinViz

Source: FinViz

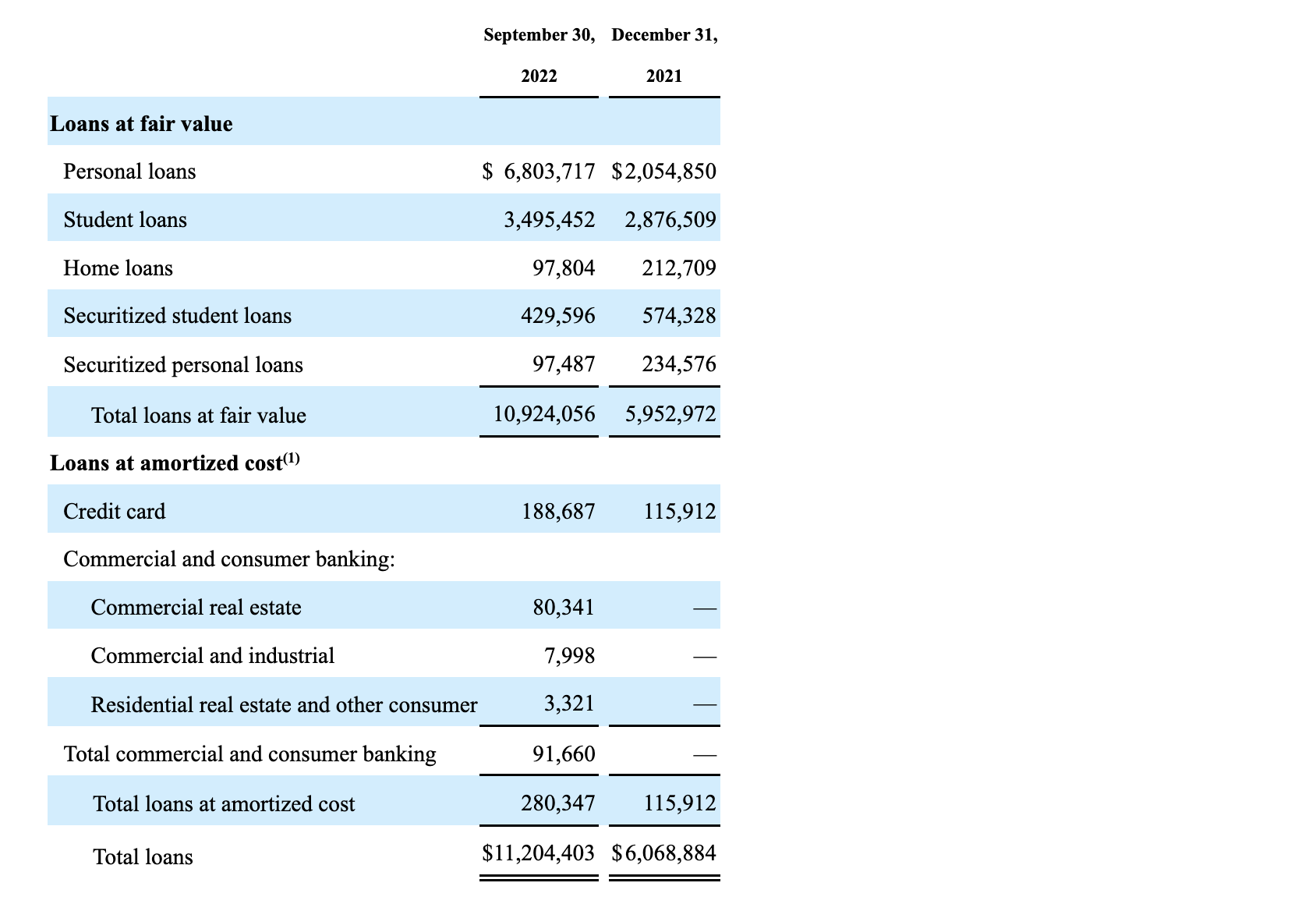

The main fear appears concerns over the loss provisions taken by SoFi with more loans held on the balance sheet in this difficult economic environment. The fintech ended the quarter with $11.2 billion worth of outstanding loans on the balance sheet held for sale, up from $6.1 billion at the end of December.

Source: SoFi Q3’22 10-Q

Source: SoFi Q3’22 10-Q

The primary concern is the higher personal loan balance at $6.8 billion, up 240% from just the end of December. SoFi only took a meager provision for credit losses of $16.3 million during Q3’22. If the fintech was actually holding the loans for investment, the digital bank would have to take a far larger credit charge.

One only has to look at LendingClub (LC) to understand the scenario facing SoFi. The Current Expected Credit Losses (CECL) charge is a relatively new Financial Accounting Standards Board (FASB) accounting standard requiring financial institutions to take a large upfront charge to cover future loan losses on new loans. The problem with this charge is that it no longer matches the financial benefits with holding loans with the credit costs.

When LendingClub took over Radius Bank, the company switched the business to investing in up to 25% of loan originations requiring a large upfront CECL charge. As an example, the fintech took a large $35 million charge in Q2’21 and $20 million in revenue deferrals leading the company to make the following explanation about the extra costs via the earnings call:

Tom will provide details, but it’s important to note that as we invested in growing our loan portfolio to build this new revenue stream, we sacrificed about $54 million in potential earnings in the quarter. We did it, because we expect holding loans to eventually generate three times the earnings compared to selling them, to the near term trade off is more than worth it.

Later in the call, CFO Tom Casey went further to discuss the impact:

However, accounting standards require us to recognize expected losses when we add them for the balance sheet, and then we recognize the interest income over the life of the loan. And this is what Scott highlighted earlier in this comment, as the income from retaining consumer loans generates three times the profitability of marketplace loans. Due to this power benefit, we expect continued growth in this portfolio.

During the quarter, we reported a non-cash credit loss provision of $35 million, primarily reflecting retention of $541 million in personal and auto repay loans on the balance sheet. There were minimum charge-offs in the second quarter, and we expect charge-offs to start to normalize gradually over the remainder of 2021 as loans typically season over nine months to 12 months.

If SoFi were to change the business, the digital bank would have to take a similar charge each quarter on new originations. But to be very clear, LendingClub switched to this business model due to the attractive economics of holding loans.

SoFi taking a large upfront non-cash charge doesn’t make the loans less attractive. What determines whether the loans are more or less attractive are the ultimate net returns after any charge-offs.

The fintech was already set to benefit from the Biden Administration ending the moratorium on student loan debt as of January 1. A U.S. judge in Texas blocking the President’s plan to provide up to $20,000 in loan forgiveness to student borrowers appears to be the final nail in the coffin.

District Court Judge Mark Pittman said the program usurped the power of Congress in making laws. With President Biden having no authority to forgive student debt, the program would appear all but dead on arrival.

As reinforced by CEO Anthony Noto on the SoFi Q3’22 earnings call, the Biden Administration student debt forgiveness plan wasn’t set to impact the business anyway. The issue all along was the end of the moratorium on repaying debt.

We think the addressable market for student loan refinancing is quite large even with these changes. Many of the forgiveness programs will probably not be applicable to our member base and our target demographics, the income levels below, for qualification, our income is higher than the income level we have to be below, and a number of other factors that would cause the TAM to be still large. Now that TAM can increase and decrease, depending on where federal funds rates are and overall WACC is for that product in the marketplace, but the number of people that will still have federal student loans outstanding that could refinance is really large still.

The student loan forgiveness plan excluded the normal SoFi member with income in excess of $125,000. The fintech guided up revenues for 2022 by a minimal $90 million amounting to a Q4 revenue boost by ~$58 million.

The stock has a minimal market cap of $5.0 billion while analysts forecast revenues surging 33% to $2.05 billion. As discussed in the previous research, SoFi should be back on path for substantial EBITDA growth with the original 2023 target after obtaining the digital bank charter at $718 million. Even half this target would triple the 2022 target of up to $120 million.

The key investor takeaway is that SoFi is far too cheap with the stock trading at ~15x conservative adjusted EBITDA targets. Investors shouldn’t fear SoFi ultimately taking CECL charges due to the loans held for investment producing higher returns per information from a peer.

The stock is too cheap at this valuation with revenues growing at twice the adjusted EBITDA multiple alone.

If you’d like to learn more about how to best position yourself in undervalued stocks mispriced by the market during the 2022 sell-off, consider joining Out Fox The Street.

The service offers model portfolios, daily updates, trade alerts, and real-time chat. Sign up now for a risk-free, 2-week trial to start finding the next stock with the potential to generate excessive returns in the next few years without taking on the outsized risk of high-flying stocks.

This article was written by

Stone Fox Capital launched the Out Fox The Street MarketPlace service in August 2020.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in SOFI over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Before buying or selling any stock, you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal.